Back to Blog

Beware of the Out-of-Market Period when transferring your MPF

For most employees, MPF contributions begin as soon as they enter the workforce and typically remain untouched until retirement at age 65, making it one of the longest-term investments in many people’s lives. Employees can manage their MPF more flexibly by consolidating or transferring their MPF accounts, allowing them to tailor their MPF investments to their personal needs.

However, like other investments, the MPF carries risks. Employees should treat the MPF as a long-term investment tool and avoid managing it with a short-term, speculative mindset. In particular, when transferring your MPF funds, they must be mindful of potential out-of-market period during the transition process.

Out-of-market period primarily refers to periods during the MPF investment process when, due to market fluctuations or fund transferring, an investor’s funds are temporarily out of the market. For example, when a member transfer MPF funds, there may be an “out-of-market period,” during which the original fund has been sold, but the new fund has not yet been purchased. During this time, market prices may fluctuate, potentially leading to a “sell low, buy high” scenario, which could negatively impact investment returns.

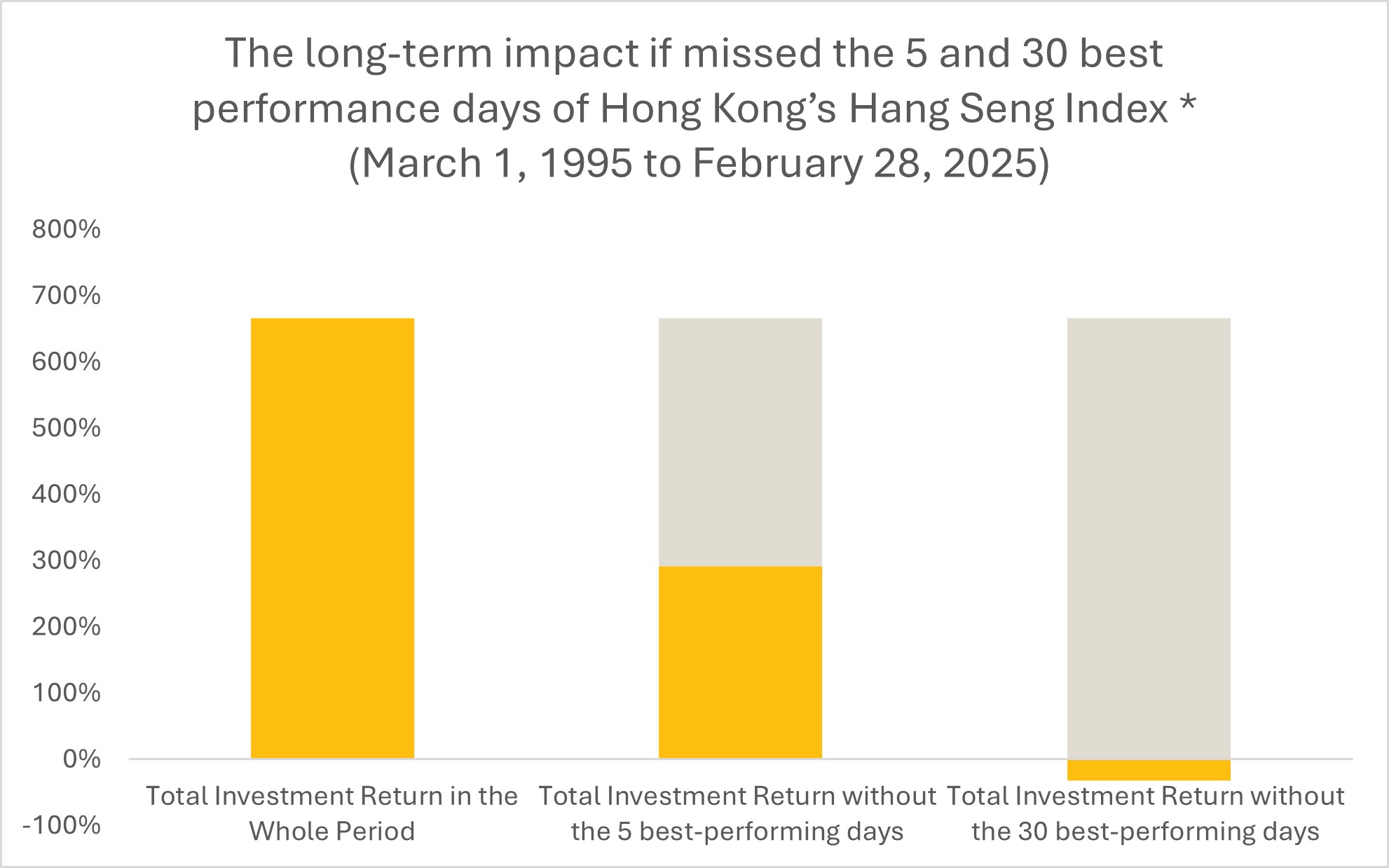

In fact, using the historical performance of Hong Kong’s Hang Seng Index as an example, from March 1995 to February 2025, the total investment return was 666%*. However, if an investor missed the 5 best-performing days of the Hang Seng Index during this period, the potential long-term return would drop significantly to just 292%, a reduction of more than half. Missing the 30 best-performing days would even turn a profit into a loss, resulting in a 32% loss. (See the chart below.)

*Source: Bloomberg, Sun Life Asset Management (data as of February 28, 2025, calculated in local currency).

Therefore, during volatile market conditions, investors should remain calm. As the MPF is a long-term investment spanning decades, employees should avoid making hasty investment decisions based on short-term market fluctuations. Doing so could lead to market timing risks and potentially result in significant losses.

Disclaimer: The information, data, and documents provided on this website are for general reference purposes only and should be used as self-help tools. Investment involves risks, and unit prices may fluctuate. Past performance figures shown are not indicative of future performance. BestServe Financial Limited and its content providers are not responsible for any loss or damage caused by reliance on any information or advice made in this website.

eMPF Tips | eMPF is Coming: Stay Calm and Gear up for a Stress-Free Transition

The transition to the eMPF platform stands out as the most critical focus in MPF market. Launched by the MPFA in June 2024, this comprehensive online platform provides a one-stop solution for managing approximately 11 million MPF accounts across Hong Kong.

Continue

Easy Steps for Fund Transfer: Learn More about Employee Choice Arrangement (ECA)

MPF transfers involve switching investment portfolios within the same scheme, or transferring MPF to another scheme. This article, we will focus on the Employee Choice Arrangement (ECA).

Continue

Enjoy Taxe Benefits and Accumulate Your Retirement Savings with MPF Tax Deductible Voluntary Contributions (TVC)

Introduced in 2019, TVC allows members to make additional voluntary MPF contributions while enjoying tax deductions. Under the current tax system, you can claim tax deduction of up to HK$60,000 per tax year. At the highest tax rate of 17% (for the 2023/24 tax year), this could result in savings of up to HK$10,200 in taxes. However, it’s important to note that this deduction cap applies to both TVC and qualifying annuity premiums.

Continue

Smart Strategies for MPF Withdrawal

Retirement marks a major life milestone, and understanding how to withdraw your MPF is a crucial part of your financial plan. This guide will help you navigate the essential details and make smart decisions to manage your retirement savings effectively.

Continue

Everything You Need to Know About MPF Contribution

The MPF system is a cornerstone of retirement protection for employees in Hong Kong. Understanding the contribution requirements ensures both employers and employees fulfill their responsibilities correctly and can plan effectively for the future.

Continue

Three Simple Steps to Make MPF Consolidation Easy

Life in Hong Kong is fast-paced, and managing MPF accounts is often overlooked when changing jobs. This can result in multiple MPF accounts under your name, making management inefficient and potentially affecting your investment strategy. In fact, consolidating your MPF personal accounts is straightforward—just follow these three simple steps.

Continue